Ghost assets

Why they matter and how to eliminate them

Ghost assets can be defined as any asset that is lost, stolen or unusable but is still shown as active on your fixed asset register. It is estimated that as many as 65% of fixed asset records are incomplete, inaccurate, or altogether missing while 10 to 30 percent of fixed assets are no longer owned1.

The accounting cost of ghost assets

For many companies, fixed assets represent the bulk of their investments and are prominent in the company balance sheet. If up to a third of listed assets do not actually exist and others are over or undervalued the financial costs can be significant. Insurance premiums and the company’s tax liability may be inflated unnecessarily. Capital budgeting and financial reporting will also be inaccurate.

! Overpaying taxes

! Higher insurance premiums

! Inaccurate fixed asset reporting affecting regulatory compliance

! Inability to forecast CapEx (Capital Expenditure) accurately

Operating impact of ghost assets

In addition to the costs above, ghost assets can lead to decreased productivity. An asset that only exists on paper is not much help when it is needed by staff. Likewise, an asset that does exist, but is listed in the wrong location is not only unavailable for use but also cannot be maintained properly and will lead to additional expense if it has to be purchased again.

! Assets unavailable for use when needed

! Cost of replacing assets unnecessarily

! Inability to track and manage maintenance of assets

How to eliminate ghost assets

Eliminating ghost assets from the fixed asset register and then keeping them off it is a two stage process. The first stage involves identifying and correcting historical inaccuracies. The second step is to ensure that the required processes and resources are available to prevent ghost assets re-appearing.

Get the right asset tracking software

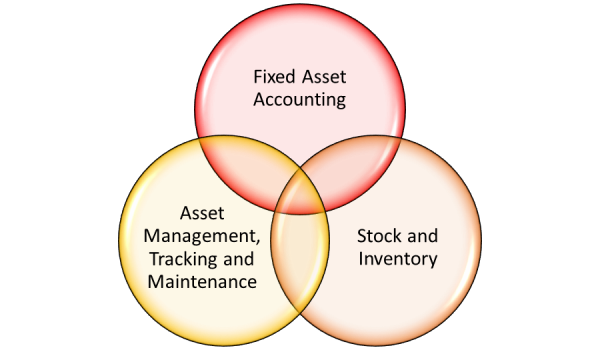

One of the most common reasons for ghost assets is a disconnect between different areas of an organisation. It is not uncommon for Finance, IT and Operations teams to each keep their own separate registers of assets and equipment. Changes to one are not always reflected in the others. Even if they are updated, changes are not made in real time and will involve a significant duplication of data and effort. An integrated asset management platform can help to prevent this disconnect by establishing a centralised asset register that is accessible to all areas of the organisation and creates a single view.

Integrated Asset Management

It is important that the solution meets the requirements of all stakeholders from the outset or it is likely to struggle to achieve the long-term buy-in required to prevent ghost assets reappearing.

Tagging and tracking assets

Barcode or RFID tagging can dramatically increase tracking accuracy and reduce the amount of time required for tracking and audits especially in larger organisations. Tagging of assets will ensure that every asset can be individually identified even when the organisation has a number of identical assets. A unique identifier (UID) means you can track individual assets across their full life cycle from purchase to disposal preventing ghost records from appearing on the register.

A number of different barcode and RFID options are available and suitable for different requirements. Some of the key factors that will influence your decision include the operating environment, number of assets and budget. For more information about selecting the right option, have a look at this comparison.

Fixed asset audits

A complete inventory of all assets and equipment is common at the start of an asset management implementation. This will give you an accurate baseline to work from going forward, but even with an integrated real time asset register as recommended above it may be necessary to conduct regular audits.

Physical inventories can be conducted concurrently at every location, this is known as “full inventory verification” or “wall-to-wall inventory.” An alternative is to carry out multiple partial inventories at different locations and within different departments, possibly at different times of year. This is known as “cyclical inventory verification”. The best method for each organisation depends on factors like available personnel and resources.

FMIS Asset Management Software provides all the functionality needed to ensure that assets are tracked and accounted for over the whole asset life cycle from purchase to disposal. Our consultants will provide the support required to help you set up the right processes and structures from the outset and to keep it that way.

If you would like to know more about FMIS Fixed Assets or any of our other solutions, please get in touch with us via email or call us on +44 (0) 1227 773003

1 Michael N. Day and Stephen Talbot, “Data Validation the Best Practice for Data Quality in Fixed Asset Management,” (White Paper) Asset Management

Resources, www.amrnow.com

https://www.fmis.co.uk/wp-content/uploads/2025/06/Feature-image-495x400-copy.webp

400

495

John de Robeck

https://www.fmis.co.uk/wp-content/uploads/2016/07/FMIS-logo-340x156.png

John de Robeck2025-06-20 15:08:202025-06-20 15:09:03FRS 102 Fixed Asset Accounting: A Practical Guide for UK Businesses

https://www.fmis.co.uk/wp-content/uploads/2025/06/Feature-image-495x400-copy.webp

400

495

John de Robeck

https://www.fmis.co.uk/wp-content/uploads/2016/07/FMIS-logo-340x156.png

John de Robeck2025-06-20 15:08:202025-06-20 15:09:03FRS 102 Fixed Asset Accounting: A Practical Guide for UK Businesses https://www.fmis.co.uk/wp-content/uploads/2025/04/Capital-Expenditure-Tariffs-495x400-1.webp

400

495

John de Robeck

https://www.fmis.co.uk/wp-content/uploads/2016/07/FMIS-logo-340x156.png

John de Robeck2025-05-14 16:20:132025-06-04 11:05:01How Tariffs Are Transforming Capital Expenditure Strategy

https://www.fmis.co.uk/wp-content/uploads/2025/04/Capital-Expenditure-Tariffs-495x400-1.webp

400

495

John de Robeck

https://www.fmis.co.uk/wp-content/uploads/2016/07/FMIS-logo-340x156.png

John de Robeck2025-05-14 16:20:132025-06-04 11:05:01How Tariffs Are Transforming Capital Expenditure Strategy https://www.fmis.co.uk/wp-content/uploads/2024/12/Depreciation-Review-495x400-1.webp

400

495

John de Robeck

https://www.fmis.co.uk/wp-content/uploads/2016/07/FMIS-logo-340x156.png

John de Robeck2024-12-18 15:04:412025-06-09 13:27:31What is a Depreciation Review and when is it needed?

https://www.fmis.co.uk/wp-content/uploads/2024/12/Depreciation-Review-495x400-1.webp

400

495

John de Robeck

https://www.fmis.co.uk/wp-content/uploads/2016/07/FMIS-logo-340x156.png

John de Robeck2024-12-18 15:04:412025-06-09 13:27:31What is a Depreciation Review and when is it needed? https://www.fmis.co.uk/wp-content/uploads/2024/12/Capital-Asset-Management-495x400-1.webp

400

495

John de Robeck

https://www.fmis.co.uk/wp-content/uploads/2016/07/FMIS-logo-340x156.png

John de Robeck2024-12-09 10:09:252025-06-09 13:31:21What is Capital Asset Management Software? (CAM)

https://www.fmis.co.uk/wp-content/uploads/2024/12/Capital-Asset-Management-495x400-1.webp

400

495

John de Robeck

https://www.fmis.co.uk/wp-content/uploads/2016/07/FMIS-logo-340x156.png

John de Robeck2024-12-09 10:09:252025-06-09 13:31:21What is Capital Asset Management Software? (CAM) https://www.fmis.co.uk/wp-content/uploads/2024/12/G-Cloud-14-approved-supplier-495x400-1.webp

400

495

John de Robeck

https://www.fmis.co.uk/wp-content/uploads/2016/07/FMIS-logo-340x156.png

John de Robeck2024-12-05 16:00:312025-06-09 13:35:55G-Cloud 14 Approved Supplier

https://www.fmis.co.uk/wp-content/uploads/2024/12/G-Cloud-14-approved-supplier-495x400-1.webp

400

495

John de Robeck

https://www.fmis.co.uk/wp-content/uploads/2016/07/FMIS-logo-340x156.png

John de Robeck2024-12-05 16:00:312025-06-09 13:35:55G-Cloud 14 Approved Supplier