FRS 102 Fixed Asset Accounting – A Practical Guide for UK Businesses

Understand how to manage fixed assets under FRS 102 with this essential guide for UK finance professionals.

Whether you’re preparing your year-end accounts or reviewing your fixed asset processes, getting to grips with FRS 102 is essential for accurate and compliant reporting. This article takes you through the key requirements of the standard, with a practical focus on how to manage your fixed assets effectively — from asset recognition and depreciation through to disposals and disclosures. It’s designed to give you the information you need to apply the standard with confidence and avoid common pitfalls.

FRS 102 provides a streamlined framework for UK businesses to manage and report on fixed assets. It sets out principles for recognising assets only when they offer future economic benefits and their cost can be measured reliably. Businesses need to differentiate between tangible assets, intangible assets, and investment properties, as each is treated differently for valuation, depreciation/ amortisation and disclosure..

Initial costs to bring an asset into working condition are capitalised, while general overheads are expensed. Companies can choose between cost and fair value models for asset valuation, but must apply a consistent approach across asset classes. Impairments, depreciation and revaluations need to be reviewed regularly to ensure accurate reporting.

Clear disclosures and consistent accounting policies are essential for transparency and compliance. Tools like FMIS Fixed Asset Accounting can support this by improving accuracy, reducing manual effort and helping firms make more informed decisions. Applying FRS 102 best practices ensures your reporting gives a true and fair view of your business’s financial position.

Whether you’re new to FRS 102 or looking to refine your asset management processes, this article explains everything from recognition criteria to disclosure requirements. With a focus on compliance, optimisation and future-proofing, it’s designed to help you improve decision-making and reporting efficiency.

FRS 102 is the principal financial reporting standard under UK GAAP, designed for medium-sized private companies, subsidiaries of larger groups, and other entities that do not apply full IFRS. Issued by the Financial Reporting Council (FRC), FRS 102 replaces a range of superseded accounting standards and brings a simplified yet robust framework aligned in part with international norms.

Any reporting entity that does not meet the criteria for micro-entity or full IFRS reporting is likely to fall under FRS 102. This includes charities, limited companies, partnerships, and groups that prepare consolidated financial statements. The standard offers a comprehensive set of principles covering recognition, measurement, presentation, and disclosure in financial statements.

FRS 102 applies to accounting periods beginning on or after 1 January 2015 and has undergone various amendments since. It is especially relevant for companies seeking consistency, compliance, and comparability in financial reporting. By simplifying the UK GAAP landscape into a single standard, FRS 102 enhances transparency in the reporting of fixed assets, financial instruments, and intangible assets, while still allowing flexibility through options like the revaluation model.

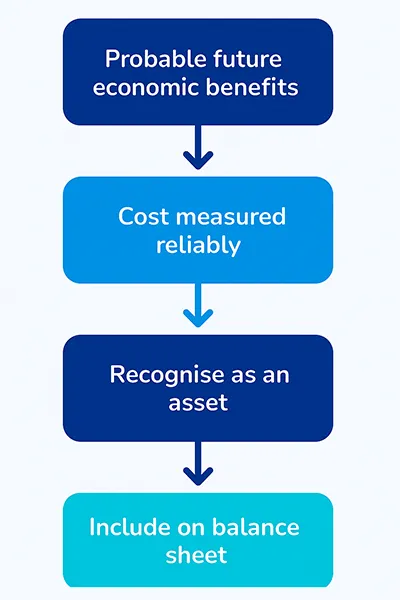

Under FRS 102, an item qualifies for recognition as a fixed asset when it is probable that the asset will provide incremental future benefits to the entity and its cost can be measured reliably. This recognition principle applies to both tangible assets (Section 17) and intangible assets (Section 18), and is consistent with the broader aim of accurate financial reporting.

Assets are typically recognised on the balance sheet at the point when the entity gains control over them, and when the asset is ready for use in the business. The recognition criteria must be assessed at each reporting date, particularly for development costs, leased assets, and subsequent expenditure.

Initial recognition should reflect all costs directly attributable to bringing the asset to its working condition. Examples include installation charges, legal fees, and delivery costs. Deferred recognition or misclassification of assets can affect the financial position and lead to compliance issues or errors in the profit and loss account.

FRS 102 defines fixed assets as assets held for use in the production or supply of goods or services, for rental to others, or for administrative purposes, and that are expected to be used during more than one accounting period. These assets fall under various categories including tangible fixed assets, intangible assets, investment properties, and assets held under finance leases.

Property, plant and equipment are typical examples of tangible fixed assets. These include land, buildings, vehicles, and machinery. Intangible assets cover non-physical resources like software, intellectual property, and development costs. The classification depends on whether the asset delivers economic benefits and can be measured reliably.

Investment properties—defined as properties held to earn rentals or for capital appreciation—are accounted for differently, often measured at fair value. Assets acquired under a finance lease are also recognised as fixed assets when substantially all risks and rewards of ownership are transferred to the entity.

Although FRS 102 does not adopt IFRS 16, it still requires that lease arrangements be assessed for classification. As such, many right-of-use assets may be considered fixed assets under the finance lease model where appropriate.

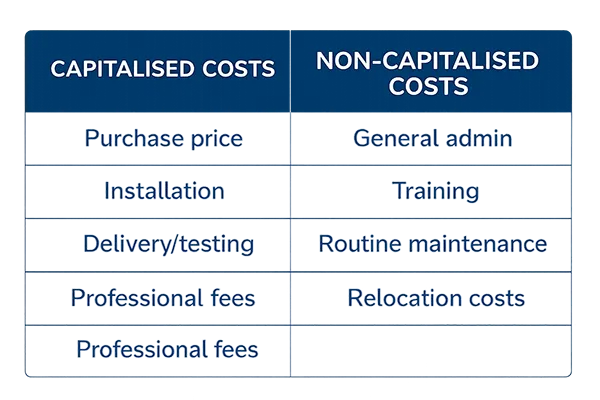

Initial recognition of a fixed asset under FRS 102 includes all costs directly attributable to acquiring the asset and preparing it for its intended use. These capitalised costs typically include the purchase price, import duties, installation, delivery, testing, and professional fees. Such costs must meet the recognition criteria of providing future economic benefits and being measured reliably.

In contrast, general administrative costs, training expenses, and relocation costs should be expensed to the profit and loss account. The correct accounting treatment of these items is essential to avoid overstating the asset’s value and misrepresenting the financial position of the business.

Subsequent expenditure on an asset should only be capitalised if it improves the asset’s performance, extends its useful economic life, or increases the asset’s capacity or efficiency. Routine maintenance and repairs are charged to the income statement as incurred.

Finance professionals must clearly document their accounting policy for capitalisation and apply it consistently across assets of the same class. This not only ensures compliance with the financial reporting standard but also supports transparent, consistent reporting.

After initial recognition, FRS 102 allows businesses to choose between two measurement models for tangible fixed assets: the cost model and the revaluation model. Under the cost model, assets are carried at cost less accumulated depreciation and any impairment losses. This is the default approach and is simpler to apply consistently across accounting periods.

The revaluation model, however, permits assets to be carried at fair value, provided this value can be measured reliably. Fair value should be determined based on market value, recent transaction prices, or professional valuation. Revaluations must be made with sufficient regularity to ensure the carrying value does not differ materially from the asset’s fair value at the balance sheet date.

FRS 102 requires that if one asset in a same class is revalued, all assets in that class must be treated the same way. Gains from revaluation are typically recognised in other comprehensive income and held in a revaluation reserve, unless they reverse a previous downward revaluation charged to the profit and loss account.

For many businesses, periodic revaluation can ensure that financial statements better reflect the real economic benefits of their assets, supporting clearer insights into the entity’s financial performance and strategic value.

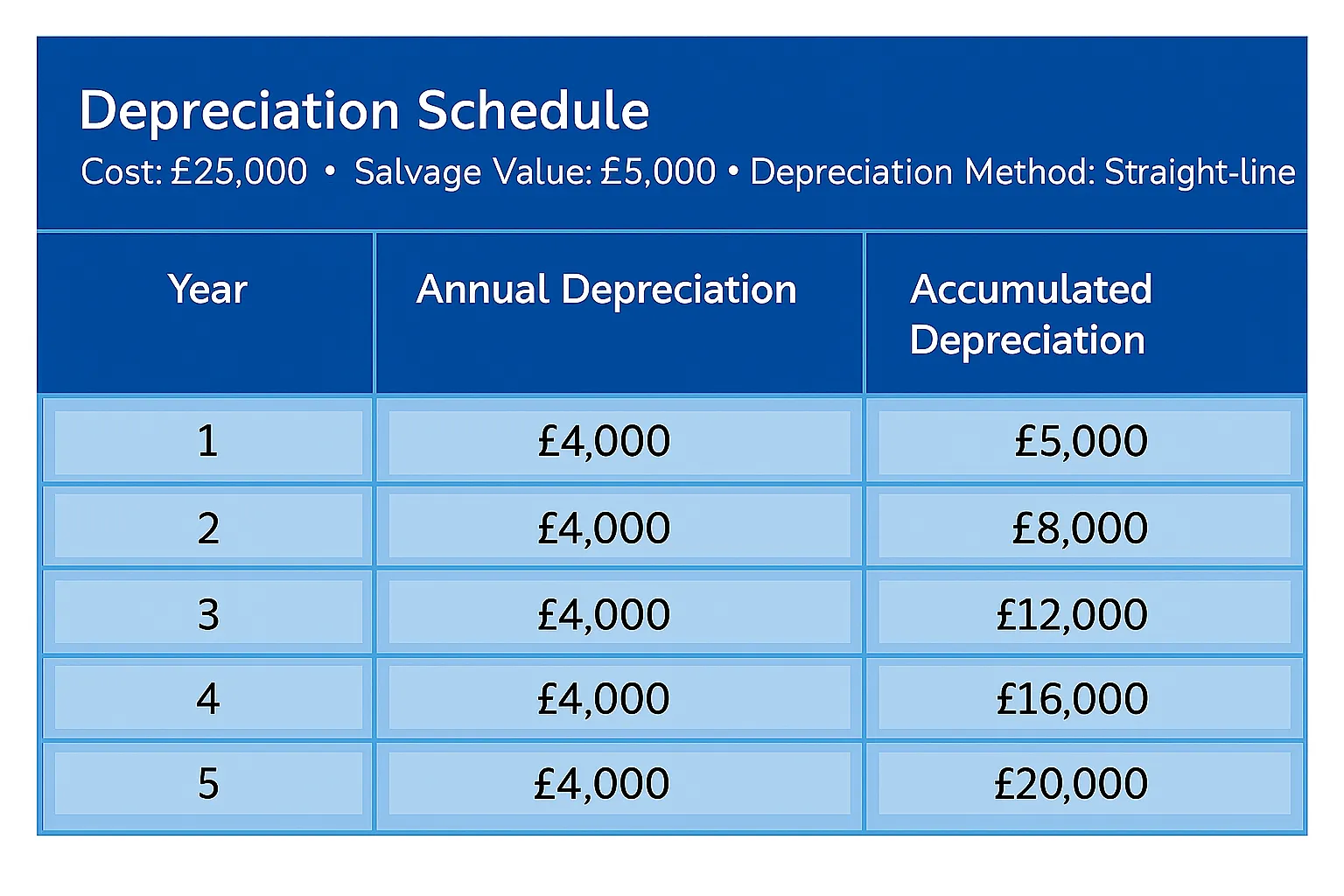

Under FRS 102, most tangible fixed assets are depreciated systematically over their useful economic life. The depreciation method used must reflect the pattern in which the asset’s future economic benefits are consumed. Common methods include straight-line, reducing balance, or units of production.

The useful life is an estimate based on expected usage, wear and tear, legal or commercial limits, and the company’s own experience. Finance professionals should regularly review these estimates, especially at each reporting date, to ensure they remain appropriate. Changes must be applied prospectively and disclosed in the financial statements.

Assets with indefinite lives (e.g. land) are not depreciated but are still subject to periodic review. Meanwhile, investment properties measured at fair value are not depreciated but are revalued annually through the profit and loss account.

FRS 102 also requires entities to assess assets for indicators of impairment. If an asset’s carrying value exceeds its recoverable amount—the higher of fair value less costs to sell and its present value of expected cash flows—an impairment loss must be recognised immediately. These losses affect both the balance sheet and the comprehensive income statement.

Investment properties are properties held to earn rental income or for capital appreciation, rather than for use in production or administrative operations. FRS 102 (Section 16) permits these to be measured at fair value at each reporting date, with changes recognised directly in the profit and loss account, not in comprehensive income.

This approach removes the need for depreciation and aligns the reported value with current market conditions, offering a more relevant view of financial performance. However, if fair value cannot be measured reliably without undue cost or effort, the cost model must be applied instead, depreciating the asset over its economic life.

Entities must disclose key assumptions and valuation methods in their financial statements. It’s also critical to ensure consistency in valuation across assets in the same class and to document the rationale behind any shift between models or valuation updates.

Correct classification is equally important. Properties used for both investment and operational purposes must be separated or treated in line with their predominant use. For example, a building partly rented and partly owner-occupied may require apportioning between investment property and property, plant and equipment.

FRS 102 requires extensive disclosures about fixed assets to ensure transparency and comparability in financial statements. These disclosures cover asset classes, valuation methods, depreciation, impairment, and any significant assumptions or accounting policies used.

Entities must provide a reconciliation of the carrying value at the start and end of each reporting period, showing additions, disposals, revaluations, depreciation, and impairment losses. This helps users of the accounts understand the asset’s performance and changes during the period.

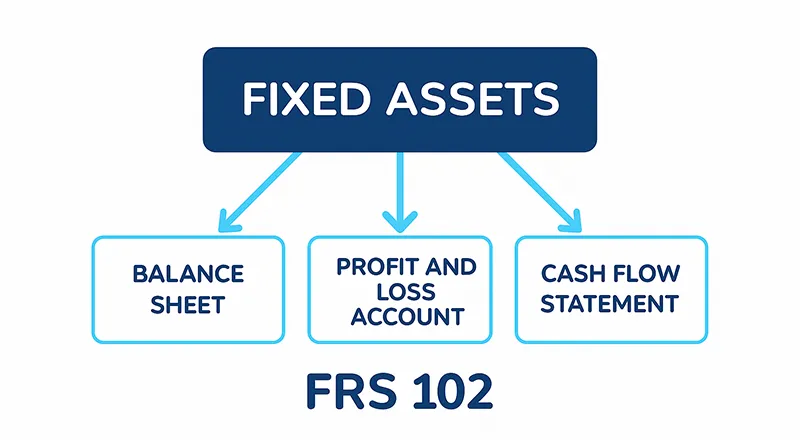

The balance sheet must reflect the net book value of each major asset class. In the income statement or profit and loss account, depreciation and any impairment losses should be clearly disclosed. If a cash flow statement is prepared, fixed asset purchases and disposals must be included under investing activities.

For investment properties, companies should disclose the basis for fair value measurement, the assumptions used, and whether an independent valuation was obtained. If fair value is not applied, reasons must be clearly documented.

Such disclosures are not merely compliance requirements; they help stakeholders evaluate the entity’s asset base, capital strategy, and expected economic benefits. Well-structured notes to the accounts support clearer understanding and enhance the credibility of the entity’s reported financial position.

To maintain strong financial control and reporting quality, finance professionals should follow several best practices when managing fixed assets under FRS 102. First, ensure all asset acquisitions and disposals are recorded promptly and that supporting documentation is retained. This includes purchase orders, invoices, and installation records that support recognition and valuation.

Asset registers should be regularly updated and reconciled to the general ledger. This helps prevent misstatements in the financial statements and ensures accurate calculation of depreciation and revaluations. Clear accounting policies should be documented and applied consistently to all assets of the same class.

It is also crucial to schedule routine reviews of asset lives, depreciation methods, and impairment triggers, especially near each reporting date. Applying these principles diligently will reduce audit risks and support better financial decision-making based on the true economic benefits the assets provide.

Using an automated system like FMIS Fixed Asset Accounting helps streamline these tasks. The software allows accurate tracking, valuation, and reporting of fixed assets, helping businesses stay compliant, save time, and generate reliable data for strategic planning.

FRS 102 provides a structured framework for the recognition, measurement, and disclosure of fixed assets, helping UK businesses improve compliance, accuracy, and strategic asset management. By following the principles outlined in this guide—covering asset recognition, capitalisation, valuation, depreciation, and disclosure—finance professionals can ensure that their financial statements reflect a true and fair view of the company’s financial position.

Implementing best practices and the right tools, such as FMIS Fixed Asset Accounting, empowers businesses to manage their asset lifecycle efficiently and confidently meet their reporting obligations.

To find out how FMIS can support your fixed asset strategy, get in touch with our team:

https://www.fmis.co.uk/wp-content/uploads/2024/03/SoftwareSuggest-Awards-2024-495x400-1.webp

400

495

John de Robeck

https://www.fmis.co.uk/wp-content/uploads/2016/07/FMIS-logo-340x156.png

John de Robeck2024-03-26 10:29:322025-06-26 07:36:38SoftwareSuggest Awards – FMIS recognised for easy implementation

https://www.fmis.co.uk/wp-content/uploads/2024/03/SoftwareSuggest-Awards-2024-495x400-1.webp

400

495

John de Robeck

https://www.fmis.co.uk/wp-content/uploads/2016/07/FMIS-logo-340x156.png

John de Robeck2024-03-26 10:29:322025-06-26 07:36:38SoftwareSuggest Awards – FMIS recognised for easy implementation https://www.fmis.co.uk/wp-content/uploads/2023/10/Asset-Valuation-Methods-495x400-1.jpg

400

495

John de Robeck

https://www.fmis.co.uk/wp-content/uploads/2016/07/FMIS-logo-340x156.png

John de Robeck2023-10-26 13:16:202025-02-13 16:03:40Asset Valuation Methods

https://www.fmis.co.uk/wp-content/uploads/2023/10/Asset-Valuation-Methods-495x400-1.jpg

400

495

John de Robeck

https://www.fmis.co.uk/wp-content/uploads/2016/07/FMIS-logo-340x156.png

John de Robeck2023-10-26 13:16:202025-02-13 16:03:40Asset Valuation Methods https://www.fmis.co.uk/wp-content/uploads/2019/06/Feature-image-495x400.jpg

400

495

John de Robeck

https://www.fmis.co.uk/wp-content/uploads/2016/07/FMIS-logo-340x156.png

John de Robeck2019-12-18 11:23:412025-02-13 16:02:50FMIS announces new NHS partnership

https://www.fmis.co.uk/wp-content/uploads/2019/06/Feature-image-495x400.jpg

400

495

John de Robeck

https://www.fmis.co.uk/wp-content/uploads/2016/07/FMIS-logo-340x156.png

John de Robeck2019-12-18 11:23:412025-02-13 16:02:50FMIS announces new NHS partnership https://www.fmis.co.uk/wp-content/uploads/2019/11/Govmoney2019-495x400.jpg

400

495

John de Robeck

https://www.fmis.co.uk/wp-content/uploads/2016/07/FMIS-logo-340x156.png

John de Robeck2019-12-02 17:25:102025-02-13 16:02:56FMIS to sponsor GovMoney 2019

https://www.fmis.co.uk/wp-content/uploads/2019/11/Govmoney2019-495x400.jpg

400

495

John de Robeck

https://www.fmis.co.uk/wp-content/uploads/2016/07/FMIS-logo-340x156.png

John de Robeck2019-12-02 17:25:102025-02-13 16:02:56FMIS to sponsor GovMoney 2019